The Energy Buyer's Guide | 09.30.2024

Natural gas futures extend gains, with benchmark pricing rising for the fifth straight week

Download the Energy Buyer’s Guide for full commentary and data relating to the U.S. and regional natural gas and power markets:

- Prompt-month natural gas futures were higher for the fifth consecutive week, as the market continued to push higher surrounding the October NYMEX expiration.

- The natural gas storage surplus is now at its lowest level since January after yet another lighter-than-average storage build of 47 Bcf during the week ended September 20.

- Spot natural gas and power prices were firmer across most of the country for the second straight week, reflecting the increasing bullishness in forward markets.

- Weather patterns are expected to moderate in the East, while the West and Midcontinent look poised to remain much warmer than normal going into mid-October.

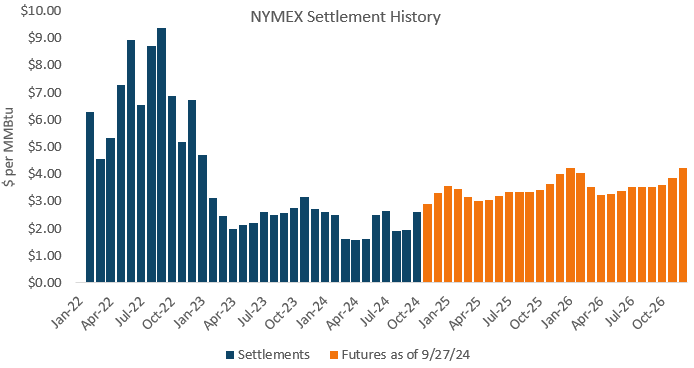

Natural gas futures were higher again last week, as the month-long price recovery continued. The October 2024 NYMEX contract expired on Thursday at $2.585 per MMBtu. This marked an increase of 65 cents, or 34% from the September expiry a month prior and brought the 2024 average to date up to $2.146 per MMBtu. The prompt-month contract has now traded higher for five consecutive weeks, while Winter 2024-25 and Summer 2025 each notched their second straight week of significant gains. Each of these seasonal strips posted its highest weekly settlement since early July. Gains were less pronounced further across the curve, as the contango was further depressed with last week’s price action.

Market sentiment has palpably shifted since the peak summer months. With weather-related demand moderating, the tight underlying balance is becoming more apparent. Storage inventories during the first three weeks of September increased by 145 Bcf, which is 49 Bcf lower than the volume added during the same period in 2023. While part of the year-over-year tightness can be chalked up to lingering heat across the Midwest and East, lower domestic production is contributing as well. Estimated output so far this month is lagging last year by more than 2 Bcf per day. Production started to rise in September 2023, but that pattern has not repeated itself in 2024. The next two months will be critical in demonstrating whether or not the market will be able to count on a surge in supply akin to the pattern observed leading up to last winter. If so, it will likely help to keep futures pricing in check in most winter weather scenarios. If not, the market’s potential for upside risk this winter will be exaggerated with supply at an ongoing deficit to year-ago levels. Until we see more concrete evidence of a ramp up in domestic production, we maintain a bullish outlook for the 12-month period and recommend end users maintain defensive fixed positions.