Natural Gas Storage: +55 Bcf

Build was in line with market expectations but lagged historical benchmarks by a wide margin.

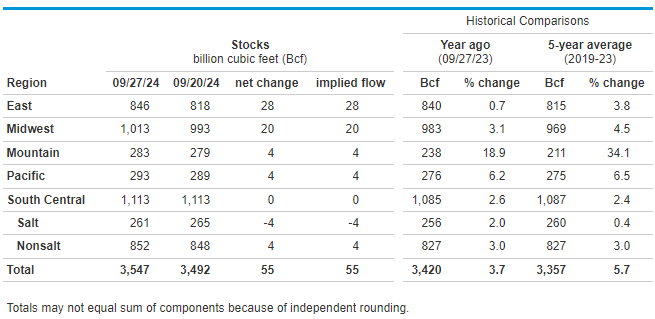

The U.S. Energy Information Administration reported a weekly injection of 55 Billion Cubic Feet (Bcf) in Lower 48 natural gas storage inventories for the week ending September 27, 2024 (Link). Total inventories now stand at 3,547 Bcf, 127 Bcf (3.7%) above year-ago levels and 190 Bcf (5.7%) above the 2019-2023 average for the same week.

Today’s storage report showed a build of 55 Bcf, which further narrowed the surplus to last year and the five-year average. Inventories are typically growing at a much faster rate at this point in the season. The five-year average build for the same week was 98 Bcf, while inventories grew by 87 Bcf during the same week in 2023. However, lingering cooling demand in some key markets and sagging domestic production have worked to limit storage additions during the current shoulder season. With the recent injection lagging the year-ago number by 32 Bcf, it implies that the supply and demand balance was more than 4.5 Bcf per day tighter than the same week a year prior. The reported injection fell virtually in line with consensus market expectations, which ranged from a 49 to a 62 Bcf build and centered around a build of 56 Bcf.

The futures market has continued to exhibit strength this week. The Winter 2024-25 strip had been trading near $3.00 per MMBtu during the first half of September, but it is now up more than 10% from that level above $3.30 per MMBtu at the highest levels since early July. Meanwhile, the prompt-month November contract is testing resistance surrounding $3.00 per MMBtu this week but so far is struggling to breach that level. Prices were up prior to the report, and the as-expected nature of the data did little to alter the trajectory of the market in the 45 minutes since the release.

Following last week’s reclassification, Salt inventories in the South Central dropped by 4 Bcf, offsetting a 4-Bcf net build into Nonsalt storage levels in that region. While all individual regions maintain a surplus to last year and the five-year average, the East Region is holding above year-ago levels by the slimmest of margins and looks poised to fall to a deficit in the coming weeks.

We are currently leaving the projection for end-of-summer inventories unchanged at roughly 3.85 Tcf. Recent market tightness suggests that the risk to that forecast may be to the downside. There are only six weeks remaining in the traditional injection season, and heating demand is becoming a larger factor as the weeks pass. Barring any dramatic temperature anomalies that keep space heating needs at bay deep into November, it is looking more and more unlikely for storage levels to eclipse 3.9 Tcf or especially approach 4.0 Tcf.

Detailed Data with Updated Charts in the Natural Gas Storage Report PDF Below: