Natural Gas Storage: -30 Bcf

Storage draw comes in smaller than expected, expanding the surplus to historical benchmarks.

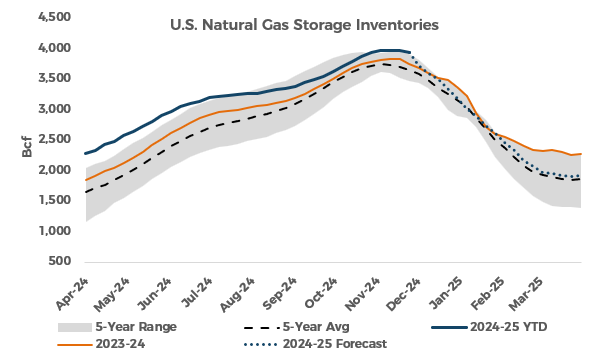

The U.S. Energy Information Administration reported a weekly withdrawal of 30 Billion Cubic Feet (Bcf) in Lower 48 natural gas storage inventories for the week ending November 29, 2024 (Link). Total inventories now stand at 3,937 Bcf, 185 Bcf (4.9%) above year-ago levels and 284 Bcf (7.8%) above the 2019-2023 average for the same week.

The EIA reported the first substantial net withdrawal of the season for the week ended November 29, with inventories declining by 30 Bcf. Compared to the 2-Bcf draw reported for the prior week, this data implies that the supply and demand balance tightened by 4 Bcf per day, week over week. Despite cooler weather impacting key markets late in the week, the draw came in light compared to historical benchmarks. The same week in 2023 was especially cold, leading to a withdrawal of 81 Bcf, while the five-year average for the week was a draw of 47 Bcf. The Thanksgiving holiday in the U.S. limited industrial and some commercial usage, skewing the magnitude of the withdrawal lower than it would have been during a typical week under the same weather conditions. Published forecasts heading into the report fell in an especially wide range, with the low-end calling for a draw of 30 Bcf and some analysts calling for a deduction as high as 55 Bcf. The actual number came in at the bearish end of that range, with most models seemingly underestimating the holiday’s impact on demand.

Natural gas futures pricing was lower on the week heading into today, with prices still well below week-ago levels despite this morning’s gains. The prompt-month January 2025 contract dipped briefly below $3.00 per MMBtu yesterday before rebounding into the daily settlement. This confirmed strong support at that psychologically important price level and has led to follow-through buying activity so far today. The market response to the government storage report was muted, with market participants so far shrugging off the bearish nature of the data.

At the time of publication, the January 2025 NYMEX futures contract was trading at $3.126 per MMBtu, up $0.083 per MMBtu from yesterday’s settlement.

The most robust draws were recorded in the East and Midwest, the two regions that felt the brunt of the late-week cold snap. The Mountain Region realized a small drawdown, while Pacific inventories were unchanged on the week. The South Central registered a 9-Bcf injection, which was entirely due to a rise in Salt storage levels.

With unseasonable cold sticking around last weekend and lingering through the current week, next Thursday’s report is likely to show an especially strong storage draw. Early estimates show a sizable increase in consumption across all sectors, which could add up to a net storage draw between 150 and 200 Bcf. Temperature patterns are poised to normalize beyond the next 3 days, however, which should work to limit the burden on storage for the following two weeks. Pinebrook Energy Advisors still sees storage levels bottoming in March between 1.9 and 2.0 Tcf.

Detailed Data with Updated Charts in the Natural Gas Storage Report PDF Below: