Natural Gas Market Note | 03.03.2026

U.S. prices edge higher for the second straight day as the steep global rally continues.

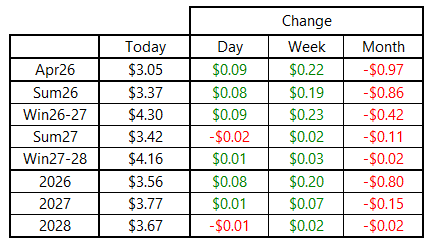

U.S. natural gas prices pushed to the upside for the second straight day, with the April 2026 contract breaking back above $3.00 per MMBtu resistance. April added 9 cents to finish the day at $3.05 per MMBtu, with gains spread evenly across the curve through Winter 2026–27. Prices were higher earlier in the session, but the market pared some of the gains into settlement to finish well off the intraday highs.

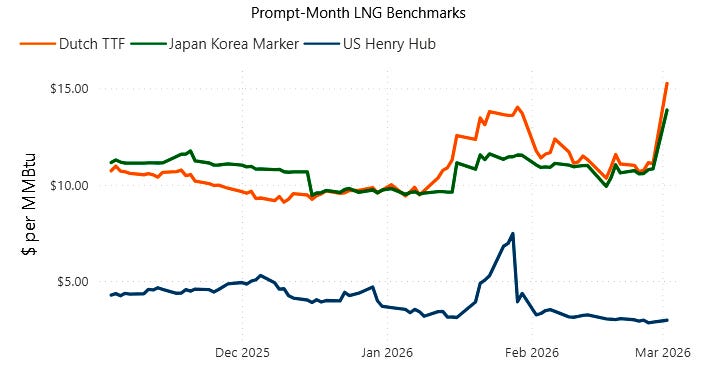

U.S. futures are up relatively modestly since the end of last week, while other global benchmarks have skyrocketed. April Dutch TTF futures were up more than 70% in two trading days, rallying from about $11 as of Friday to more than $18 per MMBtu on Tuesday. Benchmark Asian futures have seen similar gains as the reality of a potential extended supply disruption sets in.

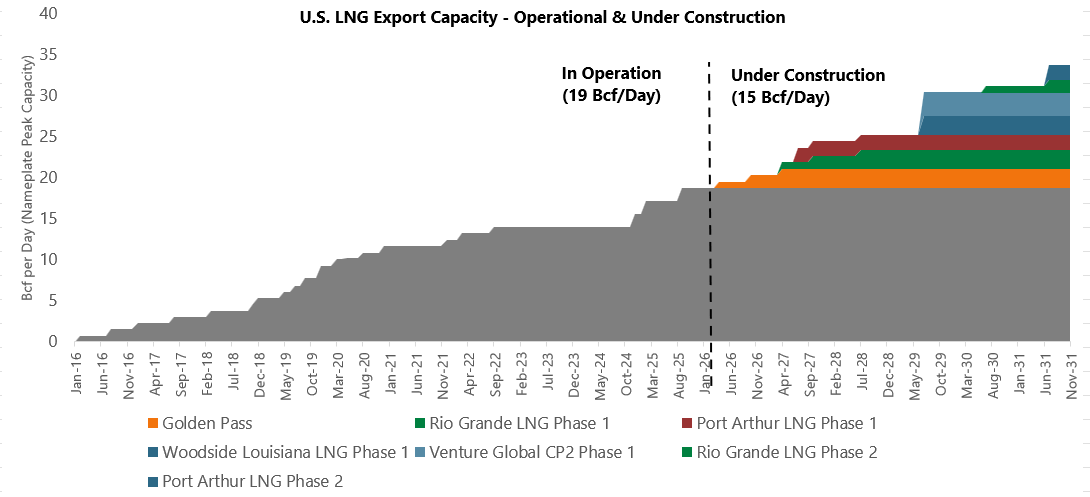

Yesterday’s closure of a major Qatari LNG export terminal, coupled with the effective closure of the Strait of Hormuz, threatens to remove about 20% of global LNG supply. While this is extremely bullish news globally, it should not have much of an impact on the U.S. market. Feedgas into domestic LNG export terminals has been averaging between 19 and 20 Bcf per day, which indicates that terminals are already running at or very close to capacity. As a result, the supply gap created by the Middle East disruptions can’t be filled by the U.S. and shouldn’t add any material demand from the LNG export sector in the near term.

However, a prolonged global price spike could lend additional urgency to U.S. terminals that are pending a final investment decision or are under construction. The Golden Pass terminal is next in the queue and had already started increasing feedgas in anticipation of entering commercial service soon. The first of three liquefaction trains will add about 0.8 Bcf per day of feedgas in March or April, with the other two trains set to come online over the following 12 months.

Beyond the 2.4-Bcf-per-day Golden Pass terminal, the other terminals that are currently listed as “under construction” have a combined capacity of more than 12.5 Bcf per day scheduled for completion over the next five years.

An archive of Daily Natural Gas Market Notes can be found here.