Natural Gas Market Note | 02.11.2026

Prices edge higher in another quiet trading session.

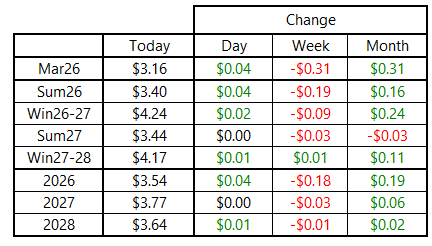

Wednesday was another relatively uneventful day in the U.S. natural gas market. Contracts were flat to higher across the curve, with the March 2026 contract rising by about $0.04 to finish near $3.16 per MMBtu. Summer 2026 edged higher by a similar margin, with deliveries beyond that nearly unchanged.

Three days into the week, the prompt-month contract has traded in a range of just $0.21 per MMBtu, from a high tick of $3.265 to a low of $3.055 per MMBtu. If this range holds through the end of the week, it would represent the lowest volatility since October. For reference, the average weekly trading range for the prompt-month contract since the start of winter has been nearly $1.00 per MMBtu — largely driven by the extreme rally and subsequent collapse surrounding the recent cold weather event.

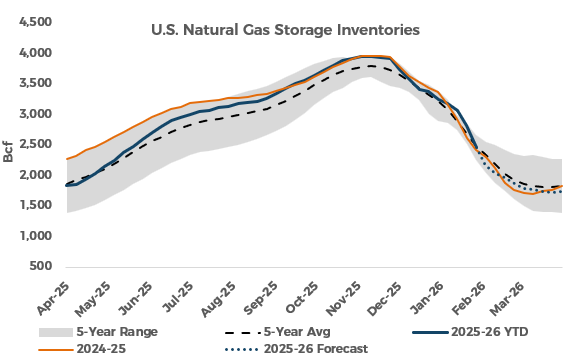

The reduced volatility this week comes as the market sees a clear end to winter risk in sight. Beyond tomorrow’s storage report, weekly withdrawals are likely to trend lower before shifting to net injections in the spring. The Wall Street Journal survey of analysts showed consensus expectations for a draw of 264 Bcf for the week ended Friday, February 6. If correct, this would cap a three-week stretch in which inventories declined by 868 Bcf, far eclipsing the previous record three-week aggregate draw of 820 Bcf set in January 2018.

However, absent any additional major cold shots, inventories should still exit the winter near year-ago and five-year average levels. Pinebrook currently projects an end-of-winter inventory level between 1.7 and 1.8 Tcf.

An archive of Daily Natural Gas Market Notes can be found here.